1. What is the Loan Payment Calculator?

Definition: The Loan Payment Calculator estimates the periodic payment, total payment, and interest paid for an amortized loan with equal payments, based on loan amount, annual interest rate, loan term, and payment frequency.

Purpose: This tool helps borrowers assess the affordability of a loan by calculating periodic payment obligations and total costs, aiding in budgeting and loan comparison decisions.

2. How Does the Calculator Work?

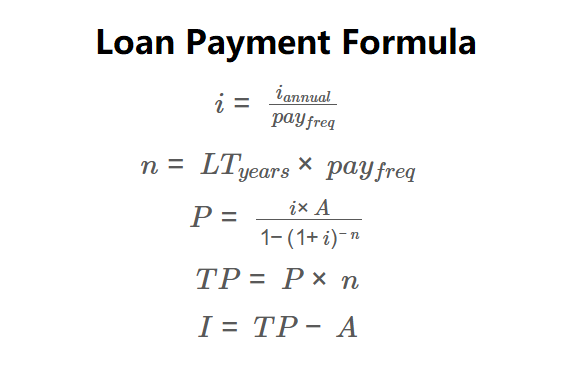

The calculator uses the following formulas:

\( i = \frac{i_{annual}}{pay_{freq}} \)

\( n = LT_{years} \times pay_{freq} \)

\( P = \frac{i \times A}{1 - (1 + i)^{-n}} \)

\( TP = P \times n \)

\( I = TP - A \)

Where:

- \( i \): Periodic interest rate (decimal);

- \( i_{annual} \): Annual interest rate (decimal);

- \( pay_{freq} \): Payment frequency (payments per year);

- \( n \): Number of payments;

- \( LT_{years} \): Loan term (years);

- \( A \): Loan amount ($);

- \( P \): Periodic payment ($);

- \( TP \): Total payment ($);

- \( I \): Interest paid ($).

Steps:

- Enter loan amount, loan term (years), annual interest rate, and payment frequency.

- Calculate periodic interest rate: \( i = \frac{i_{annual}}{pay_{freq}} \).

- Calculate number of payments: \( n = LT_{years} \times pay_{freq} \).

- Calculate periodic payment using the amortization formula.

- Calculate total payment: \( TP = P \times n \).

- Calculate interest paid: \( I = TP - A \).

- Display results in currency format.

Note: This calculator assumes an amortized loan with equal payments, where interest is calculated on the remaining principal after each payment.

3. Importance of Loan Payment Calculation

Calculating loan payments is essential for:

- Budget Planning: Determines periodic payments to ensure they fit within monthly budgets.

- Cost Management: Estimates total interest paid, helping compare loan offers and assess long-term costs.

- Financial Decision-Making: Assists in deciding whether to take a loan, choose a shorter term, or make extra payments to reduce interest.

4. Using the Calculator

Example: Calculate the payments for a $10,000 loan with a 6% annual interest rate, 5-year term, and monthly payments:

- Loan Amount (\( A \)): $10,000;

- Loan Term (\( LT_{years} \)): 5 years;

- Interest Rate (\( i_{annual} \)): 6% (\( i = 0.06 / 12 = 0.005 \));

- Payment Frequency (\( pay_{freq} \)): 12;

- Number of Payments (\( n \)): \( 5 \times 12 = 60 \);

- Periodic Payment (\( P \)): \( \frac{0.005 \times 10000}{1 - (1.005)^{-60}} \approx 193.33 \);

- Total Payment (\( TP \)): \( 193.33 \times 60 \approx 11599.80 \);

- Interest Paid (\( I \)): \( 11599.80 - 10000 = 1599.80 \);

- Result: Periodic Payment: $193.33; Total Payment: $11,599.80; Interest Paid: $1,599.80.

5. Frequently Asked Questions (FAQ)

Q: What is a periodic payment?

A: The periodic payment is the fixed amount paid regularly (e.g., monthly) to cover both principal and interest on an amortized loan.

Q: How does payment frequency affect the loan?

A: More frequent payments (e.g., monthly vs. annually) reduce total interest by paying down the principal faster.

Q: How can I reduce interest paid?

A: Choose a shorter loan term, make extra principal payments, or secure a lower interest rate to minimize total interest costs.

Loan Payment Calculator© - All Rights Reserved 2025

Home

Home

Back

Back