1. What is the Annuity Present Value Calculator?

Definition: The Annuity Present Value Calculator computes the present value of a series of regular payments, accounting for interest, compounding frequency, payment frequency, annuity type, and optional growth rate.

Purpose: Helps investors, retirees, and financial planners determine the current worth of future annuity payments for investment or retirement planning.

2. How Does the Calculator Work?

The calculator uses the following formulas based on the annuity type and conditions:

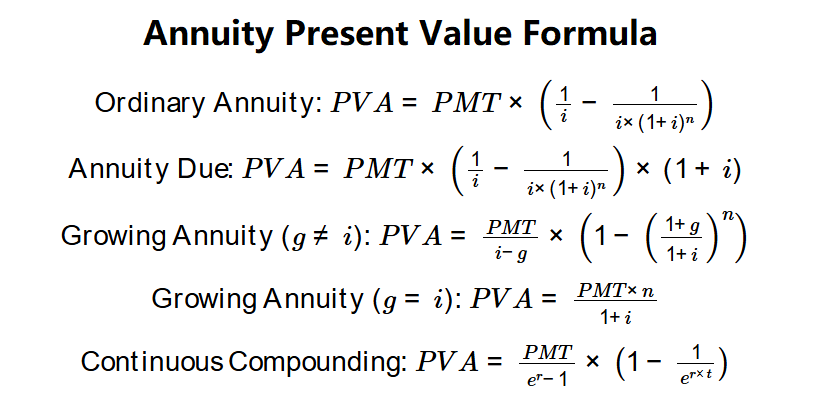

Formulas:

\(\text{Ordinary Annuity: } PVA = PMT \times \left( \frac{1}{i} - \frac{1}{i \times (1 + i)^n} \right)\)

\(\text{Annuity Due: } PVA = PMT \times \left( \frac{1}{i} - \frac{1}{i \times (1 + i)^n} \right) \times (1 + i)\)

\(\text{Growing Annuity (} g \neq i \text{): } PVA = \frac{PMT}{i - g} \times \left( 1 - \left( \frac{1 + g}{1 + i} \right)^n \right)\)

\(\text{Growing Annuity (} g = i \text{): } PVA = \frac{PMT \times n}{1 + i}\)

\(\text{Continuous Compounding: } PVA = \frac{PMT}{e^r - 1} \times \left( 1 - \frac{1}{e^{r \times t}} \right)\)

Where:

- \( PVA \): Present value of the annuity ($)

- \( PMT \): Payment amount per period ($)

- \( i \): Periodic interest rate (\( r / m \))

- \( r \): Annual interest rate

- \( g \): Growth rate per period

- \( n \): Total number of payment periods (\( m \times t \))

- \( m \): Compounding frequency per year

- \( t \): Number of years

- \( e \): Exponential constant (~2.718)

Steps:

- Step 1: Input Payment Amount. Enter the periodic payment (e.g., $1000).

- Step 2: Input Interest Rate. Enter the annual interest rate (e.g., 5%).

- Step 3: Input Number of Years. Enter the duration of the annuity (e.g., 10 years).

- Step 4: Select Compounding Frequency. Choose monthly, quarterly, annual, or continuous compounding.

- Step 5: Select Payment Frequency. Choose monthly, quarterly, or annual payments.

- Step 6: Select Annuity Type. Choose ordinary (end of period) or due (beginning of period).

- Step 7: Growing Annuity (Optional). Enable growing annuity and input growth rate (e.g., 2%).

- Step 8: Calculate. Compute the present value using the appropriate formula.

3. Importance of Annuity Present Value Calculation

Calculating the present value of an annuity is crucial for:

- Retirement Planning: Determines the current worth of future retirement income streams.

- Investment Analysis: Evaluates the value of annuity products or structured payments.

- Financial Planning: Supports budgeting by assessing the cost of future cash flows today.

4. Using the Calculator

Example:

Payment amount = $1000, Interest rate = 5%, Number of years = 10, Compounding = Monthly, Payment = Monthly, Type = Ordinary, Growth rate = 0:

- Step 1: \( PMT \) = $1000.

- Step 2: \( r \) = 0.05.

- Step 3: \( t \) = 10.

- Step 4: \( m \) = 12.

- Step 5: \( q \) = 12.

- Step 6: Type = Ordinary.

- Step 7: \( g \) = 0.

- Step 8:

- \( i = 0.05 / 12 \approx 0.004167 \), \( n = 10 \times 12 = 120 \), \( PVA = 1000 \times \left( \frac{1}{0.004167} - \frac{1}{0.004167 \times (1 + 0.004167)^{120}} \right) \approx 94,713 \).

- Result: Present value = $94,713.00.

This shows the present value of the annuity.

5. Frequently Asked Questions (FAQ)

Q: What is the difference between ordinary annuity and annuity due?

A: Ordinary annuities have payments at the end of each period, while annuities due have payments at the beginning, increasing the present value due to earlier discounting.

Q: Why include continuous compounding?

A: Continuous compounding represents the theoretical maximum frequency, useful for precise financial modeling.

Q: Can this calculator handle negative growth rates?

A: Yes, but negative growth rates are uncommon and may significantly reduce the present value.

Annuity Present Value Calculator© - All Rights Reserved 2025

Home

Home

Back

Back